DGB solves the very practical and real challenges of man’s symbiosis and relationship with trees to harness free market forces and the access to capital needed to rapidly accelerate the reforestation of earth. Here you find the most Frequently Asked Questions (FAQ) about our business model and sector.

What are nature-based solutions?

The world needs a range of measures to limit carbon dioxide (CO2) emissions while meeting rising energy demand. They include the protection and restoration of natural ecosystems such as forests, grasslands and wetlands. Nature-based solutions are the management and use of land for tackling social and environmental challenges. Nature conservation, afforestation, reforestation, agroforestry and urban greening are all land based projects which qualify as nature-based solutions.

What is a carbon offset?

Individuals and corporations around the world are recognizing the importance of reducing their GHG emissions. As a result, many of them are reducing their carbon footprints through energy efficiency and other measures. Quite often, however, it is not possible for these entities to meet their targets or eliminate their carbon footprint, at least in the near term, with internal reductions alone. They need a flexible mechanism to achieve these aspirational goals and enter the carbon markets.

By using the carbon markets, entities can neutralize, or offset, their emissions by retiring carbon credits generated by projects that are reducing GHG emissions elsewhere. Of course, it is critical to ensure, or verify, that the emission reductions generated by these projects are actually occurring.

Companies and private individuals are interested in contributing to their living environment. In order to translate this willingness into implementation, nature offsets and especially carbon offsets make nature compensation easy and provide an appropriate, flexible system of compensation.

Although there is an interest in contributing to nature conservation from the point of view of corporate social responsibility (CSR), this interest has seen a rise in the last year due to the need to reduce and offset carbon emissions. Carbon offsetting happens on a mandatory basis, as well as on a voluntary basis for Corporate Social Responsibility (CSR) and public relations.

What is a biodiversity offset?

A biodiversity offset is an innovative approach to quantify transparently the net positive impacts of an investment on 1 hectare preserved, restored, or managed through sustainable land practices. It will allow business to invest in projects that add value to the company and create tangible benefits for a region of land and its communities.

Compensating damage to nature or biodiversity is a way by which the harmful impact that an activity or intervention has upon it, can be mitigated.

Biodiversity offsetting happens on a mandatory basis, as well as on a voluntary basis for Corporate Social Responsibility (CSR) and public relations.

What does it mean ‘to retire an offset’?

By “retiring” a carbon offset or biodiversity offset on behalf of its clients, DGB removes the offsets from the market, rendering them unusable by the heavy-polluting companies. To “retire” a carbon offset, DGB officially registers the offset as “used”. Until a carbon offset is retired, it is available for trading and cannot be used to offset emissions of the current holder.

How does DutchGreen verify its offsets?

DutchGreen verifies its carbon offsets according to the VCS Program Rules. The VCS Program is the world’s most widely used voluntary GHG program. Nearly 1,700 certified VCS projects have collectively reduced or removed more than 630 million tonnes of carbon and other GHG emissions from the atmosphere.

Projects developed under the VCS Program must follow a rigorous assessment process in order to be certified. VCS projects cover a diverse range of sectors, including renewable energy (such as wind and hydroelectric projects), forestry (including the avoidance of deforestation), and others.

The VCS Standard lays out the rules and requirements which all projects must follow in order to be certified. All VCS projects are subject to desk and field audits by both qualified independent third parties and Verra staff to ensure that standards are met and methodologies are properly applied.

Projects are assessed using a technically sound GHG emission reduction quantification methodology specific to that project type.

How does DutchGreen make sure that a project has an actual impact?

DGB checks all its projects for additionality, permanence and non-leakage.

- Additionality: Additionality requires the forest project to sequester more carbon than in a ‘business as usual’ scenario. Project must demonstrate that the carbon sequestration would not have happened without the development of the specific offset project.

- Permanence: Permanence requires that GHG removal enhancements must be maintained for up to 100 years. To demonstrate permanence each project must undergo a third-party verification of inventory reports and a site visit every six years during the life of the project (~25 years).

- Non-leakage: Leakage from carbon projects happens when GHG reductions in one area results in an unintended increase in GHG emissions in another location. Project managers must demonstrate that their project does not cause excessive leakage, essentially wiping out the increases in GHG removal from their project.

Does DGB own all the land of its projects?

There are three ways in which DGB intends to gain rights to use the land for projects.:

- Buy the land

- Lease the land

- Work together with third-party landowners

In order to make a nature-based project into a success, there is always an investment from DGB into the land. The quality of the land improves from DGB’s investment.

This does not mean that DGB is always the owner of the land. The acquisition of land is only considered if there is no other possibility to conserve nature or prevent deforestation, as it requires a large(r) upfront investment to commence a project.

What are emissions trading schemes?

Emissions trading schemes, also known as emissions allowances, are regulated markets where businesses transact certificates that allow the owner of that certificate to pollute (an externality of their business activity).

The EU Emissions Trading Scheme (ETS) is the most advanced in the world. The EU sets a limited (and annually decreasing) number of "pollution allowances" to be issued to businesses (some of which are given for free, whilst others are sold), which effectively limits (and gradually enforces a decrease in) the total emissions within the European block.

In 2021, China launched its country-wide emissions cap-and-trade system, after being postponed since 2015, and it quickly became the world’s largest. That said, it's still quite nascent, especially when it comes to its secondary trading. California runs a similar cap-and-trade system and it's one of the most developed schemes alongside Europe’s.

What is CORSIA?

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) was developed by the International Civil Aviation Organization (ICAO) and was adopted in October 2016. Its goal is to have carbon-neutral aviation growth from 2020.

The scheme is voluntary and is supposed to work until 2035 at least. The total demand for those 15 years is estimated at 2,700 million tons of CO2 equivalent in offsets

What is a cap-and-trade system?

Most carbon credits are part of cap-and-trade systems, which involve a cap on the amount of carbon dioxide companies can emit and a market system through which companies can buy, sell and trade their credits.

Companies involved in these systems receive carbon credits, so they can participate in economies that monitor and regulate carbon emissions. Usually, the government sets the emissions caps for each industry and determines the penalties for exceeding the maximum emissions levels.

Companies receive carbon credits, which allow them to emit carbon dioxide, as their allowance toward the cap, or they can sometimes purchase carbon credits at auction. The cap is the number of carbon dioxide emissions the industry is not to exceed, and the allowance is each company's share of permitted emissions.

What is a voluntary carbon market?

The voluntary markets are the overall name for all voluntary verified carbon emission reduction offsets. The main objective for acquiring Verified Emission Reduction (VER) credits, is to neutralize the carbon footprint, motivated mainly by Corporate Social Responsibility (CSR) and public relations.

The voluntary carbon market enables private investors, governments, non-governmental organizations, and businesses to voluntarily purchase carbon offsets to offset their emissions. Companies that are unable to reduce their emissions can purchase carbon offsets from verified suppliers to offset their emissions.

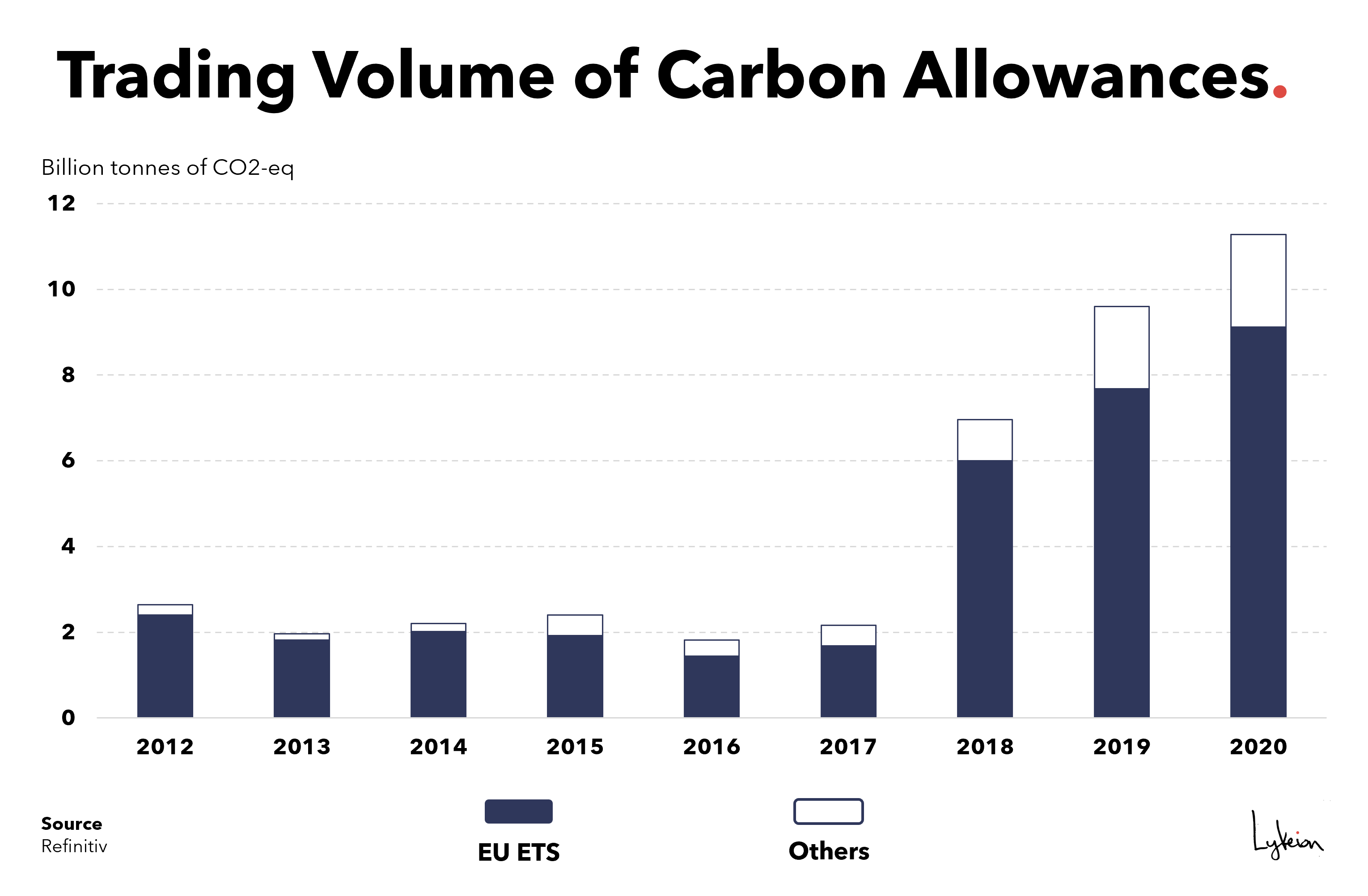

How big are the regulated ETS in comparison to the voluntary carbon market?

Regulated trading schemes cover a larger amount of carbon emissions with fewer parties involved when compared to the voluntary carbon markets. Last year the value of global carbon markets hit a record of EUR 229 billion, a five-fold increase from 2017 and the fourth consecutive year of record growth.

In 2020, the EU ETS issued over 1,300 allowances of 1mt of CO2 each (for a total of 1.3 billion tonnes). The newly created Chinese ETS was worth 4 billion tonnes. In the same year, the voluntary carbon market issued over 220 million high-quality carbon credits of 1t of CO2 each. In 2020 around EUR 1 billion-worth of carbon offsets changed hands a day.

ETSs cover larger polluters and therefore cover a more representative volume of emissions (i.e. 1.3-1.5 billion tonnes in the ETS space vs. 0.22 billion tonnes in the voluntary market), and the voluntary markets involve more parties (you and me as a consumer, a small business owner, a large retail company, etc.) and therefore a greater number of emissions certificates.

What do analysts say about the future size of the voluntary carbon markets?

As efforts to decarbonize the global economy increase, demand for voluntary carbon credits could continue to rise. Based on stated demand for carbon credits, demand projections from experts surveyed by the TSVCM, and the volume of negative emissions needed to reduce emissions in line with the 1.5-degree warming goal, McKinsey estimates that annual global demand for carbon credits could reach up to 1.5 to 2.0 gigatons of carbon dioxide (GtCO2) by 2030 and up to 7 to 13 GtCO2 by 2050.

Depending on different price scenarios and their underlying drivers, the market size in 2030 could be between $5 billion and $30 billion at the low end and more than $50 billion at the high end. while the voluntary carbon market's primary market is expected to be worth up to €100 billion by 2030.

The Taskforce on Scaling Voluntary Carbon Markets (TSVCM), sponsored by the Institute of International Finance (IIF), estimates that demand for carbon credits could increase by a factor of 15 or more by 2030 and by a factor of up to 100 by 2050.

What is the price for a carbon offset on the voluntary carbon market?

The price of 1 ton of carbon differs per offset and changes depending on the underlying projects. The main factors to establish the price of a carbon offset are:

- Type (Afforestation/Reforestation, Avoided Conversation or Improved Forest Management)

- Vintage (year of offsetting)

- Additionality (Additionality requires the forest project to sequester more carbon than in a ‘business as usual’ scenario. Project must demonstrate that the carbon sequestration would not have happened without the development of the specific offset project.)

- Location

- Community aspects

- Biodiversity aspects

The biggest difference is between avoidance type offsets and removal type offsets. Both of these offsets are extremely important for nature conservation – avoidance offsets ensure the existence of more emission-efficient businesses, while removal offsets increase the Earth’s sequestration capabilities beyond our natural wild forests and gardens.

What companies are offsetting their carbon emissions through the voluntary carbon markets?

DutchGreen is making a call to businesses and organizations worldwide to take collective action on nature, biodiversity and ecosystem restoration. The Group urges everyone to work together to build a safe and healthy planet for the next generations.

DGB envisions a connected world where collaboration among leading businesses and organizations can help conserve our precious planet and wildlife.

Below we have outlined great case studies of companies that are offsetting their carbon emissions through the voluntary carbon markets:

What is likely to drive demand for voluntary carbon credits?

Demand for lower-quality credits will decrease as more scrutiny comes into this space and people become better informed. This is an important positive development and will mean that voluntary carbon credit pricing is likely to increase as demand will focus on high-quality offsets. That will especially be the case for high-quality vetted projects in developed countries.

What is the Taskforce on Scaling Voluntary Carbon Markets?

The Taskforce on Scaling Voluntary Carbon Markets is a private sector led initiative working to scale an effective and efficient voluntary carbon market to help meet the goals of the Paris Agreement.

The Taskforce was initiated by Mark Carney, UN Special Envoy for Climate Action and Finance; is chaired by Bill Winters, Group Chief Executive, Standard Chartered; and is sponsored by the Institute of International Finance (IIF) under the leadership of IIF President and CEO, Tim Adams. Annette Nazareth, senior counsel at Davis Polk and former Commissioner of the US Securities and Exchange Commission, serves as the Operating Lead for the Taskforce. McKinsey & Company provides knowledge and advisory support.

The TSVCM’s over 250 member institutions, represent buyers and sellers of carbon credits, standard setters, the financial sector, market infrastructure providers, civil society, international organizations and academics. An advisory board of 20 environmental NGOs, investor alliances, academics and international organizations provide guidance on TSVCM recommendations.

The Task Force's unique value proposition has been to bring all parts of the value chain to work intensively together and to provide recommended actions for the most pressing pain points facing voluntary carbon markets.

How can verification and transparency of offsets drive market demand?

Carbon offsetting on a voluntary basis could be a game changer, providing funding to projects that avoid and remove carbon from the atmosphere. Yet there is scope to improve transparency of various carbon crediting mechanisms and a need for standardization of crediting and accounting. This would enhance customer trust in the offsets offered, result in higher market volumes and a real, functioning market. Large customers but also national and supranational governments should demand more standardization and regulation of this market to make this a reality in the near-term.

How does DGB harness technology?

DGB is committed to a high-tech approach to nature restoration, harnessing the latest smart technologies to secure the best outcomes for the business, its customers and, ultimately, the planet.

Every stage of its nature restoration projects will benefit from this approach; from detailed analysis at the start, to using specialised machines to mechanically speed up the planting of biodiverse species, to monitoring plant growth with drones and satellite imagery.

Sources:

- Shell: Nature-Based Solutions

- Verra: Validation & Verification

- Verra: Methodologies

- EU Emissions Trading System (ETS) data viewer

- McKinsey: A blueprint for scaling voluntary carbon markets to meet the climate challenge

- MSN: IIF sees huge potential for voluntary carbon credits, predicts $100 billion a year market by 2050

- Rabobank: Can voluntary carbon markets change the game for climate change?